{kind=link}

In the green fertile landscapes of south-western Ghana, oil palm farming has long been the backbone of rural livelihoods. Shedding light on existing oil palm marketing arrangements and their welfare outcomes reveals a story that is both promising and challenging. So, is a prosperous future for these farming communities possible? Our forthcoming publication in Oxford Development Studies, reveals our findings.

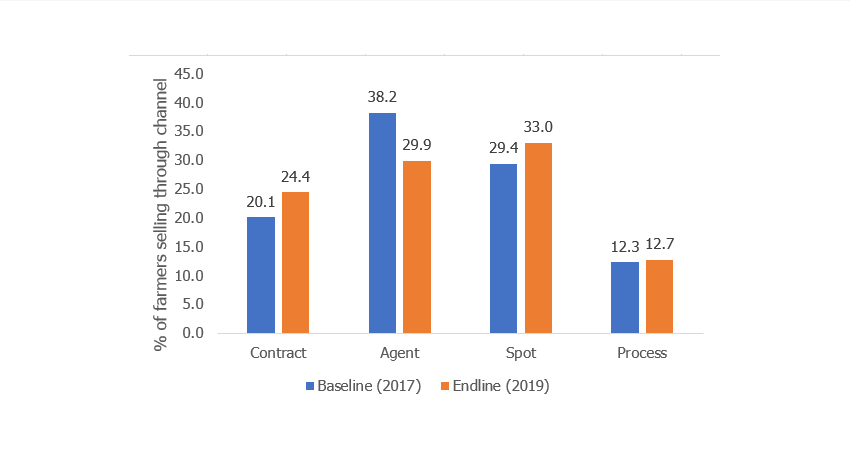

Oil palm marketing channels in south-western Ghana

One might assume that smallholders in this region, endowed with the presence of two of Ghana’s ‘big four’ industrial oil palm companies, would thrive through formal contracts with these giants. Surprisingly, our findings paint a different picture. The reality is that formal contractual relationships between smallholders and processing companies are rare. Instead, smallholders self-select one of four primary oil palm marketing pathways:

- Direct sales to companies (with verbal contracts)

- Selling to companies through agents

- Selling on the open market (spot selling)

- Artisanal or small-scale processing

Overall, our study found that, between 2017 and 2019, selling through agents (company intermediaries) and selling on the open market were the most common marketing channels in south-western Ghana. Processing was rarely used by oil palm farmers in the area (Figure 1).

However, some shifts in farmers’ choice of marketing pathways were observed over the period. Selling through agents was the most popular channel in 2017, shifting to spot sales in 2019. Generally, over the study period, farmers shifted away from agents and were moving to one of the other three channels.

So why are farmers shying away from agents? The main reason farmers cited was perceived exploitation by agents. Farmers explained that agents often adjusted their oil palm weighing scales to cheat them, and sometimes bought produce at prices far less than factory gate prices. This perception has resulted in mistrust of oil palm buying agents in the area.

Behind the choices: destitution and constraints

Why do differences exist in marketing choices? The answers are grounded in the stark realities communities face. Household and community-level deprivation plays a pivotal role. Low incomes, low scale of production, distance from industrial oil palm companies, and limited access to mechanised processing equipment are all barriers for contract and processing channels. In addition, other factors including cash flow/prompt payments, presence of adult females in the household (a determinant of the choice of oil palm commercialisation), availability of daily markets and artisanal processing mills, and road infrastructure contribute to marketing choices. For instance, spot market sales dominate in communities that are far away from oil palm companies, but which have daily markets.

Moreover, collective arrangements, where resources are pooled to transport harvests to company mills improve prices, yet these arrangements often collapse due to the breakdown of trust and the inability of poor farmers to meet their commitments. Sadly, this means that the most marginalised farmers, who could benefit the most from collective action, are excluded from these arrangements.

Divergent pathways to profits

The choice of marketing channels are not just a matter of convenience; they hold significant implications for household welfare. Households engaged in their own processing who then sell directly to industrial companies are significantly better off. Households with marketing contracts enjoy significant yearly welfare premiums, equivalent to US$912 and US$1,006 compared to households using agent and spot market channels, respectively. Moreover, agent and spot market pathways lead to greater seasonal food insecurity compared to those that process their own oil palm.

We also found that oil palm commercialization pathways yield different welfare outcomes for men and women mainly because of underlying gender differences in access to resources. Broadly, male farmers in Ghana and other developing regions mostly have better access to land, labor, credit, and decision-making power, allowing them to fully capitalize on the opportunities offered by contracts and processing activities to attain better livelihood outcomes. For example, the contract farming and palm oil processing pathways are associated with higher asset accumulation for male-headed households but not for female-headed households. For the same reasons, our study also revealed that, overall, households headed by females were significantly more food-insecure than male-headed households. However, when compared to women with contracts, the women-headed households processing oil palm themselves had a significant food insecurity-reducing effect. This suggests that the choice of small-scale processing as a marketing channel is more gender-inclusive than the other choices.

A pathway to a prosperous oil palm future

Our findings elicit important policy implications for inclusive agricultural commercialization. The channels that enhanced a household’s welfare the most – direct sales to industrial companies, and small-scale processing – should be encouraged through the relaxation of entry constraints. Provision of production capital (including land, seedlings, and other inputs) would encourage smallholder farmers to expand their operations – enabling them to benefit from large-scale production gains.

In addition, expanding access to mechanized processing facilities could empower more smallholders, particularly women, to choose this option. This is especially important as oil palm processing has been shown to significantly reduce gender-related welfare gaps.

Furthermore, rural infrastructure development, particularly improved roads, could significantly reduce transaction costs and enhance engagements between smallholders and industrial processing companies.

To achieve these goals, a quasi-state agency, such as the recently established Ghana Tree Crop Development Authority, could regulate the market for ‘fresh fruit bunches’ and enforce contracts. Such a crucial institution could provide much-needed structure and regulations to ensure that smallholders benefit from the value they create in Ghana’s oil palm sector.

This blog is published from Agricultural Policy Research in Africa (APRA), a research programme of the Future Agricultures Consortium (FAC). Read the original article.

- Log in to post comments